My life may or may not consist of a series of questionable (and sometimes poorly thought out) choices that are ever so slightly outside my comfort zone. Even with a long line of shaky choices to choose from, a recent choice (and the topic of this post) might mark the climax of my personal brand of impulsive opportunism.

Since I'm wholly unable to structure my posts for dramatic effect and gave away the surprise in the title, what I'm trying to say is: I bought a house. Don't worry though, the house is 3,000 miles away and I still totally live in a truck.

Wait, what?

It's a sad fact of reality that despite having a decent job and pocketing/investing all of my rent-savings by living in a truck for the past three years, I'm not anywhere remotely near the realm of having the luxury of considering the idea of potentially almost thinking about purchasing a home in the Bay Area.

But, with that same decent job and rent-savings, I'm perfectly well-equipped to buy a home many other places in the country, including around my hometown, for example. In fact, if you squint a bit, three years of Bay Area rent is a pretty solid down payment in a lot of places. So when a close family member lamented their frequently rising rents and frustrations trying to get a mortgage, I had an idea.

My thought went something like this: I could buy a home, and they could live in it and fix it up to their liking (their significant other is a contractor, who fixes houses for a living). When they move elsewhere, I can finish paying off the mortgage in one lump payment and start renting it out, or even sell it if I so desire.

So that's what I've been up to for the past few months: making offers on homes in the Greater Boston area. About two months ago, one of my offers was accepted, and a few hectic weeks later, I flew out to Boston to sign my soul and first-born child away close the deal and help the aforementioned family member move in. It's definitely weird to say, but as of May 24th, 2018, I'm officially a homeowner. Just to reiterate, I still live in a truck though.

The Process

Not that I ever intended for it to be this way, but the blog tends to be pretty family-friendly. I mean it makes sense, I'd really have to go out of my way to make a blog about box trucks overtly risqué or indecent. Allow me to trample all over that for a brief second with some PG-13 language:

Buying a house is a f***ing process.

Not only is it a process, but (as one might expect) living in a truck and being 3,000 miles away doesn't make it any easier. If you've never bought a home (3,000 miles away) (while living in a truck) before, the process looks roughly like this:

| 1. | Find an agent. |

| 2. | Find a real estate attorney. |

| 3. | Put in offers. |

| 4. | Get offers rejected. |

| 5. | Put in more offers. |

| 6. | Get an offer accepted. |

| 7a. | Panic, existentially. |

| 7b. | Panic, financially. |

| 8. | Shop for a mortgage. |

| 9a. | Get inspections done. |

| 9b. | Be horrified at the findings of the inspections. |

| 10. | Panic again financially, for good measure. |

| 11. | Negotiate a closing credit based on inspection findings. |

| 12. | Sign the purchase + sale agreement. |

| 13. | Choose a lender, sign a million mortgage-related papers. |

| 14. | Get a loan commitment. |

| 15. | Explain to the bank that you live in a truck, but it's totally not weird. |

| 16. | Fail to convince them it's not weird, but get them to approve your mortgage anyway. |

| 17. | Fly home for the closing, sign a stack of papers that is quite literally thicker than the boards your new home is made of. |

| 18. | Breathe, deeply. |

| 19. | Be a homeowner, and |

Whew, that was a doozy. I'm convinced that buying a house is made intentionally convoluted and counter-intuitive to make it as expensive as possible. If buying a house was straight-forward, our GDP would probably plummet. At every step of the process, it feels like there's a group of used car salesmen-types eagerly waiting to take your hard-earned money, and you can't help but laugh at the literal dozens of different fees itemized at closing. I can understand why people put in "all-cash" offers on homes, and why they're so attractive (the offers, not the people making them, though I guess being rich is attractive to some people).

In any case, it's over. It's done. Salient details:

- Loan/insurance labelled as for a "second home". Because I won't be living in the home most of the time, except when I come home for holidays, none of the banks I talked to were willing to classify this as a "primary home" loan, which I find ironic, seeing as I don't have a primary home.

- ~$2,300/month mortgage payment (including tax + insurance) on a 15-year loan. For a bit of perspective, this is less than what some of my SF-based friends pay in rent. I opted for a 15-year loan, instead of a more traditional 30-year loan, because I wanted to get a better rate. I bought the house at a bad time, just after mortgage rates skyrocketed. Since I knew I'd be holding onto the loan for a while (probably the whole lifetime of the loan), I opted to optimize for lower rates, at the expense of a higher monthly payment and slightly higher closing costs.

- 20% down payment. To avoid private mortgage insurance, lock in a better rate, yada yada.

- 4.125% interest rate. Not bad, though not great compared to rates even a few months earlier. Still a significantly better rate than if it had been classified as an investment property.

- Total out of pocket: ~$80,000. I sold a bunch of my index funds to cover it. Luckily, I'd had all of them for more than a year, so I'll get to pay for the gains at the long-term rate come tax time next year. I also used the opportunity to consolidate all of my investments into the Admiral Share variants of the funds I invest in, which sometimes have slightly lower expense ratios and support buying fractional shares.

- Total home cost, after closing credit: $320,000. When discussing with my family member the price range I was willing to put in offers on, I think we agreed on $275,000 to $350,000, and this was comfortably in that price range. Though at one harrowing point in the home shopping process, I did put in a $370,000 offer on a home, nearly 10% over asking, and it was (perhaps thankfully) rejected.

- Two bedrooms, one bath. The home itself is pretty small, about 1,000 sqft. It sits on a ~9,500 sqft lot, and has a in-ground pool and a patio.

Some Hiccups

As noted above, there are a lot of moving pieces in the home-buying process, and not all of those pieces moved as smoothly as I might have liked. I'll talk about a few of the more entertaining ones.

The Clock is Ticking

Right off the bat, we had a pretty aggressive closing date, which was less than a month from the date of the offer. I'm told that this makes the offer more attractive because it means the dozens of middle-men get paid sooner the seller wants to be done with the sale as quickly as possible. This means that I had to be pretty quick in coordinating inspections and finding a mortgage and shuffling papers back and forth between interested parties, and that any subsequent hiccups had to be dealt with quickly.

Thoroughly Horrified

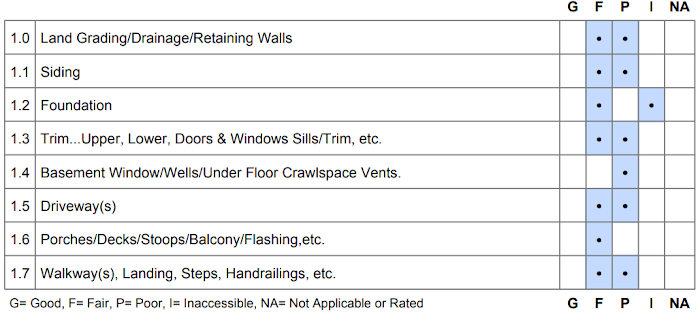

The next wrench in the works was the inspection report. In hot housing markets (like the Bay Area), buyers usually waive their right to inspections because it's so competitive. Buying a house in Massachusetts meant I had the luxury of having a home inspection performed. The inspection itself was extremely thorough, which was problematic in the sense that it highlighted an overwhelming number of problems with the home. For example:

This was the results of the "Exterior" section of the home report. You might notice that nothing was labelled as in "Good" condition, only "Fair" or "Poor". This was the general trend for other sections of the report as well, including the roof, basement, plumbing, electrical, etc. I probably shouldn't be surprised, given the house was built in the 1920s. In total, the report has 61 densely packed pages worth of findings (with pictures and diagrams and explanations, oh my!), each one enough to keep me tossing and turning at night with the specter of future home repairs looming over me.

In the end though, the problems weren't dire enough to warrant backing out of the purchase, even if I had the legal right to do so. Instead, I looked at the few most pressing and immediate repairs that would be necessary, and got some estimates for how much it would cost to fix each one. I ended up negotiating a $7,500 credit at closing (deducted from the closing costs). Originally, I had asked for a little bit more, but it turns out banks get spooked if you ask for more than a few percent of the total value of the home. C'est la vie.

The Elephant in the Room

Mortgage lenders (understandably) want to make sure you can pay back the money they're considering loaning out to you. As a matter of fact, this is so important to lenders that they have a whole department dedicated explicitly to this, called the underwriting department. They'll look at your income, assets, expenses, and various other aspects of your life to determine whether or not they think you can afford your mortgage payments for the foreseeable future. Particularly relevant to my case, they look at your current housing expenses.

When they asked me if I rent or own my current residence, I told them (in my most political voice) that I have an agreement worked out where I don't have to pay rent. It's technically true if you squint a bit, and I thought I was being pretty slick. Turns out it's their job to be slicker than I am, and indeed they are. They wanted proof of this alleged agreement, which naturally I couldn't furnish. So I had to spill the proverbial beans and tell them that I live in a truck.

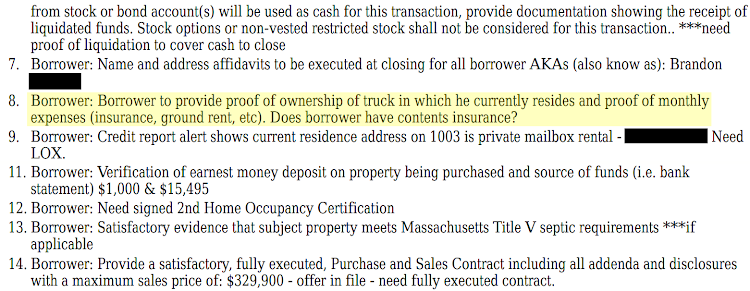

At this point, I expected them to run for the hills. What respectable lender of sound mind and functional faculties wants to put hundreds of thousands of dollars in the unwashed hands of some truck-dwelling degenerate? But the underwriting department is far more pragmatic than I had giving them credit for. Instead of abandoning ship, they simply asked for proof that I owned the truck, and proof that I had insurance on it. It was literally written into the legal paperwork:

A snippet from the loan commitment document, redacted to protect my secret identity and highlighted to draw attention to the absurdity of my life.

I provided them a copy of the title, registration, most recent insurance policy, and a link to this blog for good measure (any new readers from Citizens Bank — hello!), and the process kept on rollin' along.

Home Insurance

This last hiccup I only include because I found it interesting, and it's not something I would have expected. Mortgage lenders want to ensure their home is insured in case of catastrophic acts of man or nature. That definitely makes sense. What makes slightly less sense, is that a few home insurers I spoke with won't insure a "second home" if they aren't also insuring your first home, probably so they can get more money from you. That means if you rent your main residence (or you live in a truck), there is no way to get insurance through certain providers (cough Liberty Mutual cough) on another property. Luckily, this isn't universally true, and I was able to secure insurance on the home after a few tries.

Okay, I think that covers most of the major hiccups/wrenches (or any other metaphor for unexpected difficulties you may prefer). Now let's talk about how bad of a decision this was.

Crunching the Numbers

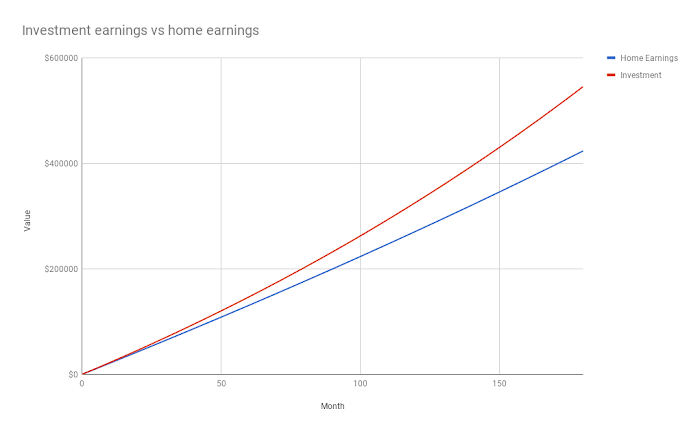

In case you wanted some visual evidence of how terrible of a decision this was from a financial perspective, here's a graph:

The larger the gap between the red and blue lines, the more money I'm hypothetically losing. With the set of arbitrary and made-up numbers I chose here, it's about ~$125,000 over the lifetime of the mortgage.

When I was trying to make sense of the finances involved, it made sense to compare buying a house with continuing to invest the money, like I've been doing. To get a sense of how the house would work as an investment, I modeled it after a hypothetical future where I could rent it out for a reasonable market rate. Here's what you're seeing:

The red line shows investment returns from what I'd have to take out to cover the down payment and closing costs, plus investing all of the money I would be spending on the mortgage every month. In terms of Excel/Google Sheets, the formula I came up with:

=FV( Investment Return Rate / 12, Months Since Starting, -Monthly Mortgage Cost, -(Down Payment + Closing Costs), 0 ) - (Down Payment + Closing Costs)

where =FV is a function for calculating the value of an investment with fixed monthly contributions (in this case, investing the money I'd otherwise be spending on the mortgage).

The blue line shows investment returns from investing a hypothetical rent ($1,800/month) minus all of the non-mortgage expenses (tax, insurance, repairs, etc), plus the non-interest portion of each mortgage payment to account for equity in the house. In terms of Excel/Google Sheets, this looks like:

=FV( Investment Return Rate / 12, Months Since Starting, -(Hypothetical Rent - Monthly Non-Principal Home Costs), 0, 0 ) + Months Since Starting * (Loan Principal / (Length Of Mortgage In Years * 12))

While this is a good ballpark estimate, there are some glaring omissions here. For example, both lines assume a constant "Investment Return Rate" of 4%, which is probably too low, but also doesn't account for any sort of capital gains taxes. Changing this to something higher, like 8%, widens the gap between the two lines. The blue line isn't accounting for depreciation/appreciation in the value of the house (which is especially hard to predict), or any of the potential tax incentives for owning a home.

In any case, the graph is moot because it assumes I'm collecting any rent, which isn't even an option since my loan is for a "second home" instead of an "investment property". That's because I decided the better interest rate was worth more than any subsidized rent would be. If I'm getting anything from the home now, it's coming from my family fixing it up, and hopefully a bit of appreciation in home value. Plus, it's hard to put a value on diversification, but I imagine it's probably good that I no longer have like 95% of my investments in stocks.

Looking Forward

An important question to ask at this point: how does all of this factor into my plans for financial independence/early retirement?

In short, it takes my plans, pulls their underwear clear over and around their head, kicks them to the ground, beats them to a pulp, sets them on fire, and snorts the ashes.

Before buying the house, my estimates for reaching financial independence were anywhere from 4-8 years. Now, I'm not really sure. A few months ago, this would have been a big deal for me, but post-quarter-life crisis, I'm less concerned with racing towards "retirement" and more focused on just living well.

If I did want to do the financial independence math, it gets a lot more fuzzy and hand-wavy now. On one hand, I took a big chunk (~25%) out of my nest egg and gave myself a fun, somewhat large, new recurring expense. On the other hand, it sets me up to have a consistent source of semi-passive income in the future.

I'm still maxing out all my tax-advantaged retirement accounts, but I'll conceivably be putting much less into my brokerage account. Having the mortgage might also inspire me to reign in some of my rampant "fun budget" spending, but who knows?

Anyway, this post is getting criminally long, so I'll just leave you with a fun fact: There are two words (not counting variations) in the English language that contain the letters m-e-o-w next to each other. One, naturally, is "meow". The other, perhaps less obviously, is "homeowner".